Similar to a study by Rogoff and Reinhart of past financial crises, Carmen and Vincent Reinhart (After the Fall, August 2010) observe that the post-crisis unwinding of a characteristically long build-up in excess credit in the decade before such crises is a serious impediment to GDP growth and employment for ten years following the crisis. In other words, the debt unwind is a slow, agonizingly long process. Because this process takes so long, the mistake that policy makers repeatedly make is to assume the after-effects of the crisis are temporary, where as the subsequent slow growth is long-term, and can be exacerbated by timid policies that neither support fiscal spending nor deal with the capital-adequacy problems of key financial institutions.

In After the Fall, the Reinharts cover 15 episodes of financial crises, including three global episodes—the 1930s Great Depression, the 1973 Oil Shocks and the 2007 Subprime Crisis, as well as Japan’s 1992 crisis. Everyone is aware that stock prices plunged during these crises, but what happened to other financial markets during the same period?

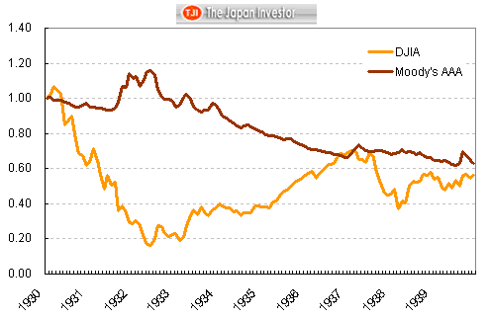

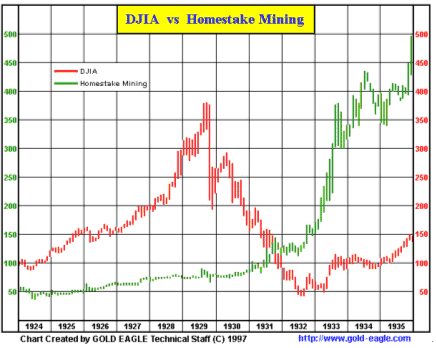

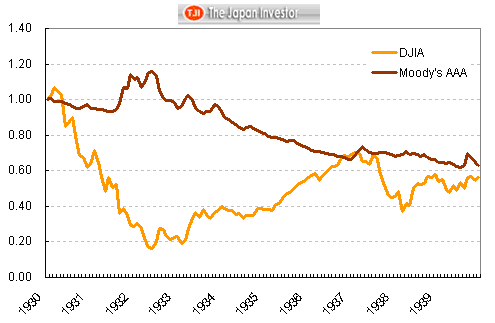

The Great Depression

click to enlarge

Source: Yahoo.com. Jan. 1930 = 1.00

Source: Gold-Eagle.com

As the above charts show, interest rates as measured by the coupon on Moody's AAA corporate bonds declined during the entire decade following the Crash of '29, as the period was characterized by strong debt deflation. On the other hand, using the stock price of Homestead Mining as a proxy for gold prices during the period, gold prices not only sold, they went ballistic, rising five-fold during the 1930 to 1939 period.

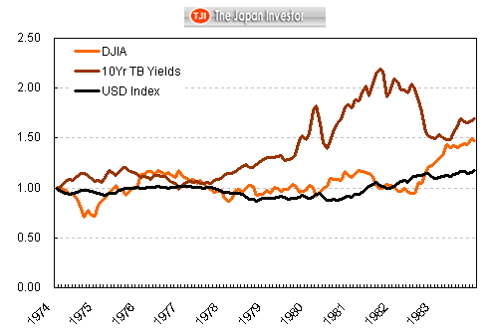

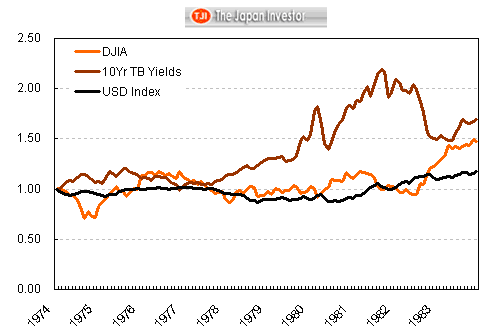

The 1970s Oil Shocks

Sources: Yahoo.com, St. Louis Federal Reserve

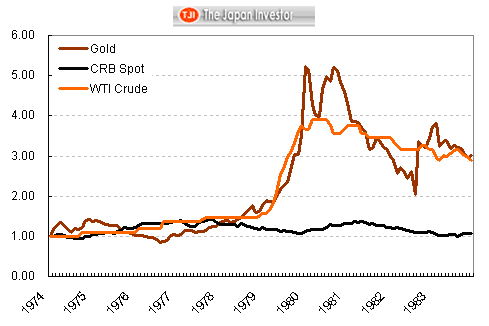

Sources: Yahoo.com, World Gold Council

In the decade after the 1973 oil shock, bond yields surged to around 1982 because of the virulent inflation unleashed by the exogenous shock to prices throughout the global economy because of the sudden interruption of crude oil supplies. Stock prices, particularly in real, inflation-adjusted terms, saw one of the worst bear markets in history, but revived and staged a strong rally as soon as bond yields began falling. On the other hand, gold prices were surging during the peak of inflationary pressures during this period, again by about 500%.

From the historical experience of these two global financial crises, those who claim gold rises both in periods of deflation and inflation are historically correct. But the major caveat is after a major financial crisis. The strong inference of course is that the real driver of gold prices during these periods was not inflation or deflation per se, but the rapid increase in government debt that debased fiat currencies and spooked investors into a strong risk-aversion mode. In other words, when it looks like the world's economy and financial markets are going to hell in a hand basket, your first choice should be to go long gold, and then worry about whether it's inflation or deflation that is the problem.

Source: Yahoo.com. Jan. 1930 = 1.00

Source: Gold-Eagle.com

As the above charts show, interest rates as measured by the coupon on Moody's AAA corporate bonds declined during the entire decade following the Crash of '29, as the period was characterized by strong debt deflation. On the other hand, using the stock price of Homestead Mining as a proxy for gold prices during the period, gold prices not only sold, they went ballistic, rising five-fold during the 1930 to 1939 period.

The 1970s Oil Shocks

Sources: Yahoo.com, St. Louis Federal Reserve

Sources: Yahoo.com, World Gold Council

In the decade after the 1973 oil shock, bond yields surged to around 1982 because of the virulent inflation unleashed by the exogenous shock to prices throughout the global economy because of the sudden interruption of crude oil supplies. Stock prices, particularly in real, inflation-adjusted terms, saw one of the worst bear markets in history, but revived and staged a strong rally as soon as bond yields began falling. On the other hand, gold prices were surging during the peak of inflationary pressures during this period, again by about 500%.

From the historical experience of these two global financial crises, those who claim gold rises both in periods of deflation and inflation are historically correct. But the major caveat is after a major financial crisis. The strong inference of course is that the real driver of gold prices during these periods was not inflation or deflation per se, but the rapid increase in government debt that debased fiat currencies and spooked investors into a strong risk-aversion mode. In other words, when it looks like the world's economy and financial markets are going to hell in a hand basket, your first choice should be to go long gold, and then worry about whether it's inflation or deflation that is the problem.

No comments:

Post a Comment